Oracle AI Cloud Strategy

Capstone Strategic Analysis

A graduate-level strategic analysis of Oracle Corporation's transformation from enterprise software incumbent into AI cloud infrastructure competitor. Applies Porter's Five Forces, VRIO, SWOT, TOWS, and Burton's strategic typology to identify where Oracle can credibly win against AWS, Microsoft Azure, and Google Cloud — and where it cannot. The central recommendation: Oracle should not try to out-scale hyperscalers. It should out-integrate them.

This project is a strategic business analysis of Oracle Corporation's position in the AI-driven cloud infrastructure industry, developed as a graduate capstone at Santa Clara University's Leavey School of Business.

Oracle is simultaneously one of the most established enterprise software companies in the world and one of the most aggressive new entrants in AI cloud infrastructure. That duality creates the strategic tension at the center of this project. The company is defending high-margin legacy database and ERP businesses while committing hundreds of billions of dollars to AI infrastructure through initiatives such as Stargate and the expansion of Zettascale AI clusters.

The question is not whether Oracle can build AI data centers. It is whether Oracle can build a defensible and profitable position in AI cloud while competitors with larger infrastructure footprints, deeper developer ecosystems, and more flexible pricing models continue to expand.

Why This Project Exists

The enterprise cloud market is being restructured by a single underlying shift. Large enterprises are no longer buying cloud compute as a commodity. They are buying AI-enabled workflows, and the infrastructure is a means to that end.

This shift exposes Oracle to a strategic inflection point. Oracle's historical advantages come from tightly integrated enterprise systems, database leadership, and long-term customer relationships. Its historical disadvantages come from smaller cloud infrastructure share, higher capital intensity relative to its revenue base, and a reputation centered on legacy enterprise software rather than modern developer platforms.

Against that backdrop, the project was designed to answer three questions:

- Where does Oracle actually have a defensible right to win in AI cloud infrastructure?

- Where is Oracle likely to lose if it competes head-to-head with hyperscalers?

- What strategic moves would credibly move Oracle from its current position into a more defensible one?

Project Scope and Approach

The analysis was structured to mirror how a corporate strategy team or management consulting firm would evaluate a company facing a large transformation decision. The work proceeded through four phases, each built on the output of the prior phase.

- External analysis. PESTEL assessment of the macro environment, Porter's Five Forces to map industry structure, and a competitive landscape scan covering AWS, Microsoft Azure, Google Cloud, IBM, and Salesforce.

- Internal analysis. Burton's strategic typology to classify Oracle's posture, value chain mapping, and VRIO assessment of Oracle's core resources and capabilities.

- Integrative analysis. SWOT consolidation, TOWS to translate findings into candidate strategies, and identification of the critical financial and operational concerns that any recommendation must address.

- Recommendations. Two short-term and two long-term strategic moves, each evaluated against Porter's generic strategies, the Five Forces, VRIO, and Miles and Snow's strategic typology to test internal coherence.

The Problem Worth Solving

Oracle's recent trajectory describes a company moving two directions at once. On one hand, the majority of its revenue continues to come from high-margin, recurring enterprise software and database contracts. On the other hand, its fastest growth, largest capital commitments, and most public announcements now center on AI cloud infrastructure, where it competes with firms several times its size.

This creates a classic strategic straddle. Burton's framework would classify Oracle as an Analyzer with Innovation, meaning the company is attempting to defend existing advantages while simultaneously pursuing new ones. Porter would describe the same situation as a risk of being stuck in the middle: neither a cost leader on raw infrastructure nor a pure differentiator on the AI stack.

The analysis concluded that Oracle cannot resolve this tension by running faster on the hyperscaler playbook. AWS and Azure have structural advantages in global infrastructure scale and developer ecosystems that Oracle is unlikely to close through capital expenditure alone. A sustained attempt to match them on generic compute would pressure margins, increase debt, and dilute Oracle's differentiation.

The more defensible path is to narrow the competitive surface, not widen it.

The Core Insight

Oracle should not try to out-scale hyperscalers. Oracle should out-integrate them.

Oracle's most durable strengths are not in infrastructure breadth. They are in the vertical integration of database, enterprise applications, and cloud into a single platform that already sits inside the mission-critical workflows of large enterprises. That integration is where switching costs are highest, where competitor imitation is hardest, and where AI is most valuable to customers, because AI is useful to enterprises primarily when it operates on trusted, governed, enterprise-owned data.

The VRIO analysis reinforces this. Two of Oracle's resources meet all four VRIO criteria at the highest level: its vertically integrated enterprise ecosystem, and its autonomous database technology. Neither is easy for hyperscalers to replicate because their platforms are optimized for open, multi-tenant commercial environments rather than end-to-end control over the database, infrastructure, and application layers.

This insight reframes Oracle's strategy. The question is no longer "can Oracle keep up in AI infrastructure." The question is "where can Oracle embed AI so deeply into the enterprise stack that hyperscalers cannot follow."

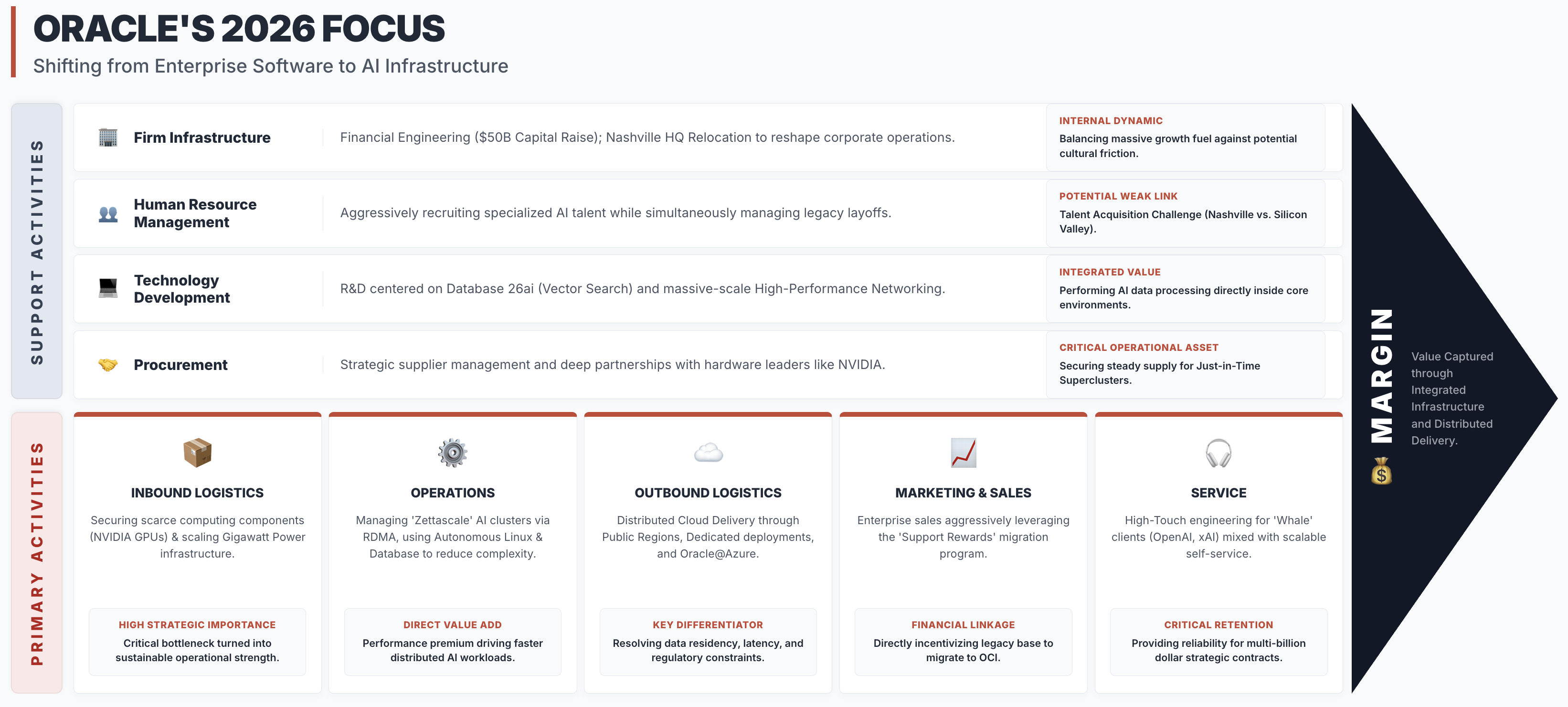

Where Oracle Fits in the AI Cloud Stack

A useful way to see Oracle's position is to map the entire AI cloud ecosystem as a stack, from silicon at the bottom to applications at the top, and mark where Oracle already plays credibly and where it would need to extend.

The progression below walks the stack layer by layer. Oracle enters at the application and cloud platform layers, where its enterprise footprint is strongest. The long-term recommendations then push Oracle deeper into orchestration and the data layer through partnerships and targeted acquisitions, and upward through model partnerships, until the company operates across every layer of the stack without needing to own each one.

Step 1. Oracle's existing strengths in Applications, SaaS, and Cloud Platforms through OCI

The point is not that Oracle should build every layer. The point is that Oracle should be present in every layer that touches enterprise data, because that is where integration creates switching costs.

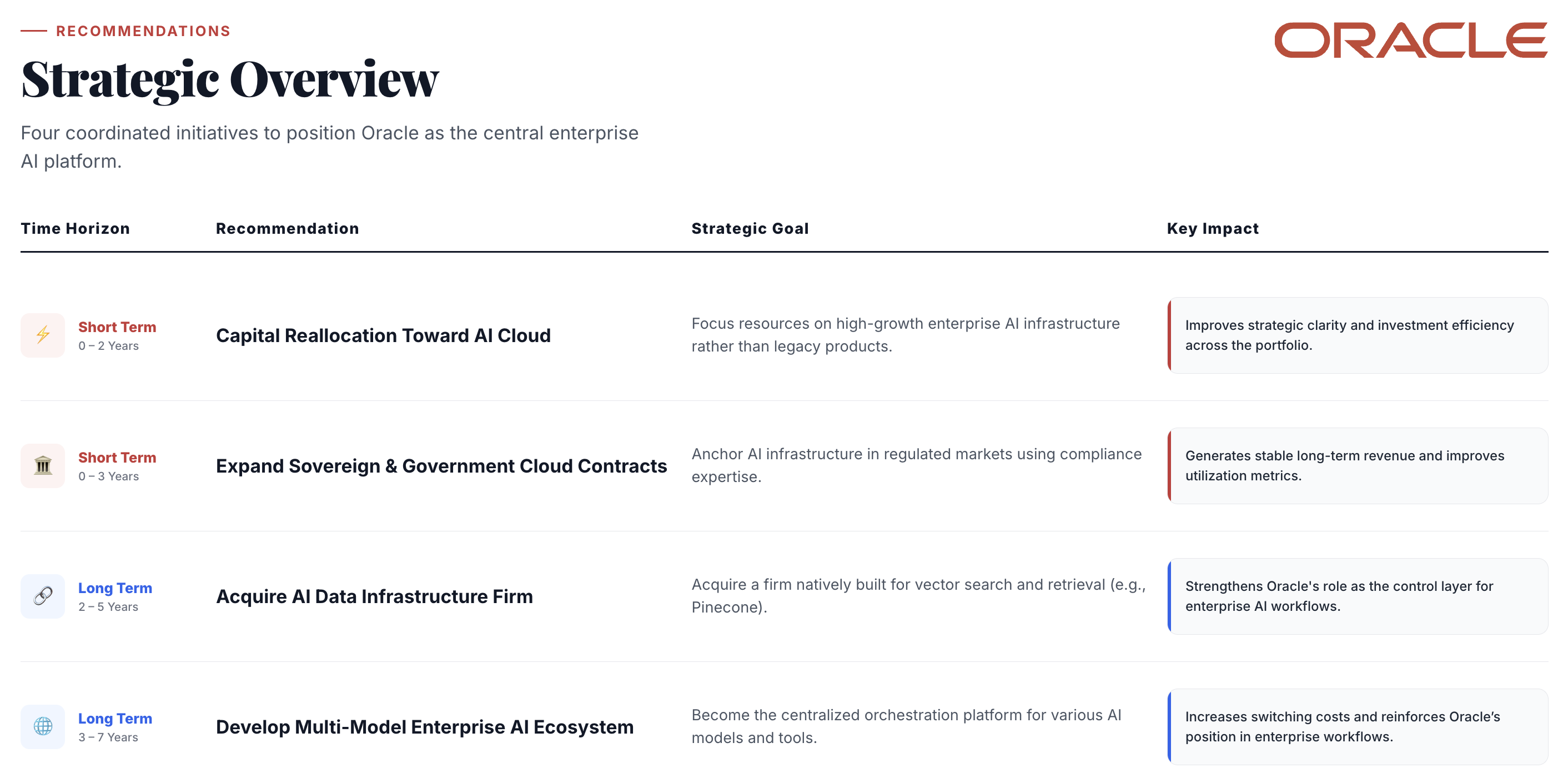

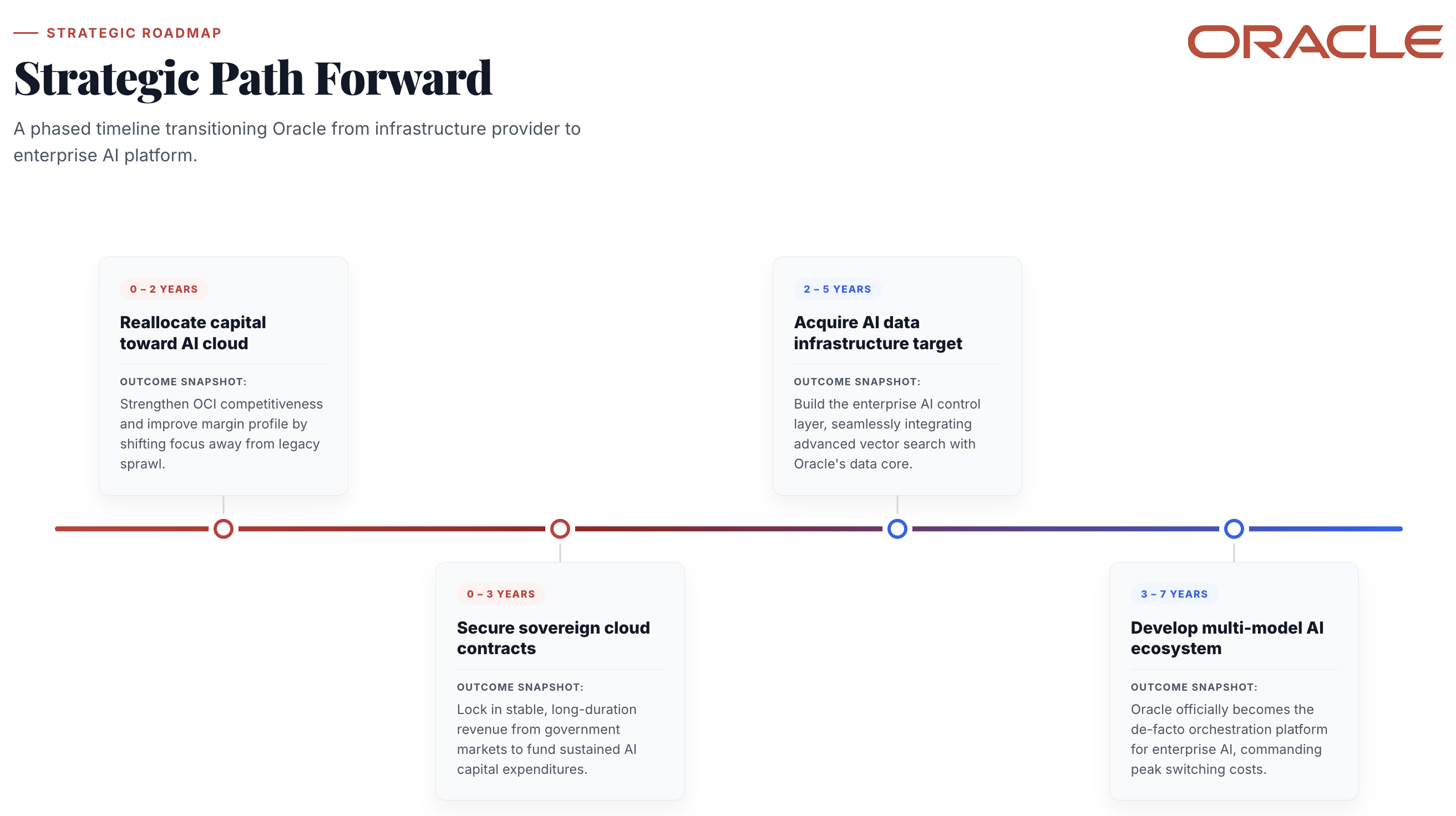

Strategic Recommendations

Four recommendations follow from this insight, structured across two short-term and two long-term horizons. Each is designed to reinforce Oracle's differentiation strategy rather than stretch it.

Short-Term 1: Reallocate Capital Toward Enterprise AI Integration

Rather than spreading investment across generic compute expansion, Oracle should concentrate capital and product investment on embedding AI directly into its existing ERP, supply chain, and human capital management applications. This moves Oracle away from strategic straddling and toward a coherent broad differentiation strategy under Porter's framework.

The effect on the Five Forces is material. A vertically integrated AI cloud platform raises switching costs because customers would have to migrate not only data but also integrated enterprise systems. That reduces the threat of substitutes and moderates buyer bargaining power at the same time.

Short-Term 2: Win Sovereign and Government Cloud Contracts

Data sovereignty, national security, and expanding digital regulation are structural forces, not passing trends. Governments and regulated industries increasingly require that sensitive data remain within national borders and be processed on infrastructure subject to domestic compliance frameworks.

This is a segment where hyperscalers are structurally disadvantaged. Their global infrastructure is designed for standardization and mass-market scalability, not locate-within-border deployment. Oracle's Cloud Infrastructure is already positioned for sovereign deployments, and its existing security certifications and government contracting experience give it a credible procurement advantage.

The recommendation extends beyond direct government agencies to adjacent organizations subject to similar compliance regimes, including defense contractors, intelligence-adjacent private firms, and international institutions governed by sovereign data requirements.

Long-Term 1: Targeted Acquisition in the AI Data Layer

Oracle's AI cloud position is strongest at the database and application layers and weakest at the AI data infrastructure layer, including vector databases, retrieval orchestration, and enterprise-grade RAG tooling. A targeted acquisition, for example a firm such as Pinecone or a similar vector database and retrieval specialist, would close this gap quickly rather than forcing Oracle to rebuild it organically.

Under Porter's framework this does not change Oracle's classification as a differentiator. It sharpens that classification. Oracle would compete on a more distinctive combination of database, ERP, governance, and AI workflow integration rather than on compute scale. Under Miles and Snow, it pulls Oracle from a loose Prospector posture back into a disciplined Analyzer posture, which better fits Oracle's financial profile and customer base.

Long-Term 2: Build a Multi-Model Enterprise AI Ecosystem

The final recommendation is to build a tightly integrated, multi-model enterprise AI ecosystem spanning database, infrastructure, and application layers. This is the end state implied by the prior three recommendations and the natural extension of Oracle's vertical integration.

A multi-model approach is deliberate. Enterprises increasingly want model optionality rather than lock-in to a single foundation model. Oracle's role is not to win the foundation-model race but to be the layer underneath it, providing the governed data, the compliant infrastructure, and the workflow integration that makes any model usable inside a regulated enterprise.

The combined effect of the four recommendations is a tightly integrated system of activities that is difficult to replicate piecewise. That is the kind of strategic position that justifies the scale of capital investment required to support Oracle's transformation.

Critical Risks and Financial Discipline

The analysis does not ignore the downside of Oracle's current trajectory.

Oracle's capital expenditures have climbed sharply, margins are under near-term pressure, and its total obligated AI cloud contract commitments have grown to levels that materially increase execution risk. The TOWS analysis surfaced this directly. The Weakness and Threat quadrant argues that Oracle must balance exploration of AI growth with disciplined exploitation of its existing high-margin businesses.

The recommendations are therefore paired with financial guardrails. Infrastructure expansion should be tied to secured multi-year contracts and sustainable operating cash flow. High-margin AI workloads should be prioritized over low-margin commodity compute services. The strategic intent is not to retreat from AI growth, but to pace it in a way that remains financially resilient if the market reprices capital-intensive AI infrastructure.

Strategic Takeaways

Three takeaways extend beyond Oracle specifically.

Scale is not always the right answer for an incumbent entering a new category. When a company enters a market dominated by larger competitors, matching them on scale tends to compress margins and blur positioning. The more defensible move is often to narrow the competitive surface until the incumbent's structural advantages dominate.

Vertical integration becomes more valuable, not less, in the AI era. Enterprise AI is only as good as the data, governance, and workflow context surrounding it. Companies that own the full stack from database to application have a structural advantage when AI is layered into existing business processes.

Strategy frameworks compound when used together. Porter, VRIO, Burton, and Miles and Snow each surface a different dimension of the same underlying problem. Used independently, each framework can justify conflicting conclusions. Used in sequence, with each stage constraining the next, they produce recommendations that are internally coherent and defensible across multiple analytical lenses.

Viewed through those takeaways, the Oracle analysis is less about Oracle and more about how established companies should evaluate entering categories defined by new technologies. The right strategic question is rarely "can we compete" but "where can we compete in a way that our competitors cannot easily follow."