Hyundai and the EV Tax Credit

Subsidy Mechanics and Strategic Response

An economics-led market analysis of how the U.S. federal EV tax credit shaped the competitive position of the Hyundai Ioniq 5, and how Hyundai's strategic response — a $7.6B U.S. assembly plant and domestic battery partnerships — restored price parity with the Tesla Model Y. The analysis applies demand- and supply-side subsidy theory, price and cross-price elasticity, and Cournot competition, then translates the findings into strategic implications for Hyundai under continued policy uncertainty.

This is a market and strategic analysis of how the U.S. federal EV tax credit has shaped the competitive position of the Hyundai Ioniq 5, and how Hyundai's response to losing — and then regaining — that incentive illustrates several core economic principles in action.

The federal EV tax credit, introduced under the Inflation Reduction Act, provides up to $7,500 to buyers of qualifying new electric vehicles. To qualify, final assembly must occur in North America. When the rules took effect, the Ioniq 5 — assembled in South Korea — lost eligibility, putting it at an immediate ~$7,500 effective price disadvantage against domestically assembled rivals like the Tesla Model Y. Hyundai's response was to relocate Ioniq 5 production to the new $7.6B Hyundai Motor Group Metaplant America (HMGMA) in Bryan County, Georgia, restoring eligibility and re-establishing price parity.

That sequence — credit introduced, Hyundai disadvantaged, $7.6B in domestic capacity built, eligibility regained, parity restored — is a clean case study in how policy-driven incentives reshape pricing power, competitive positioning, and long-run supply structure. Continued uncertainty around the credit (proposed legislation would eliminate it entirely) makes the strategic question worth examining in real time.

Background

The federal EV tax credit is a demand-side subsidy of up to $7,500 for buyers of qualifying new electric vehicles. Under the IRA, eligibility now requires final assembly in North America, with additional rules on critical minerals and battery components.

| Make & Model | Starting MSRP | MSRP Minus Tax Credit |

|---|---|---|

| Hyundai Ioniq 5 | $42,600 | $35,100 (post-relocation) |

| Tesla Model Y | $44,990 | $37,490 |

Before the move to HMGMA, the Ioniq 5 carried no effective discount, while the Model Y did — a $7,000+ effective price gap. After the move, the Ioniq 5 not only restored eligibility but became the lower effective-price option among the two.

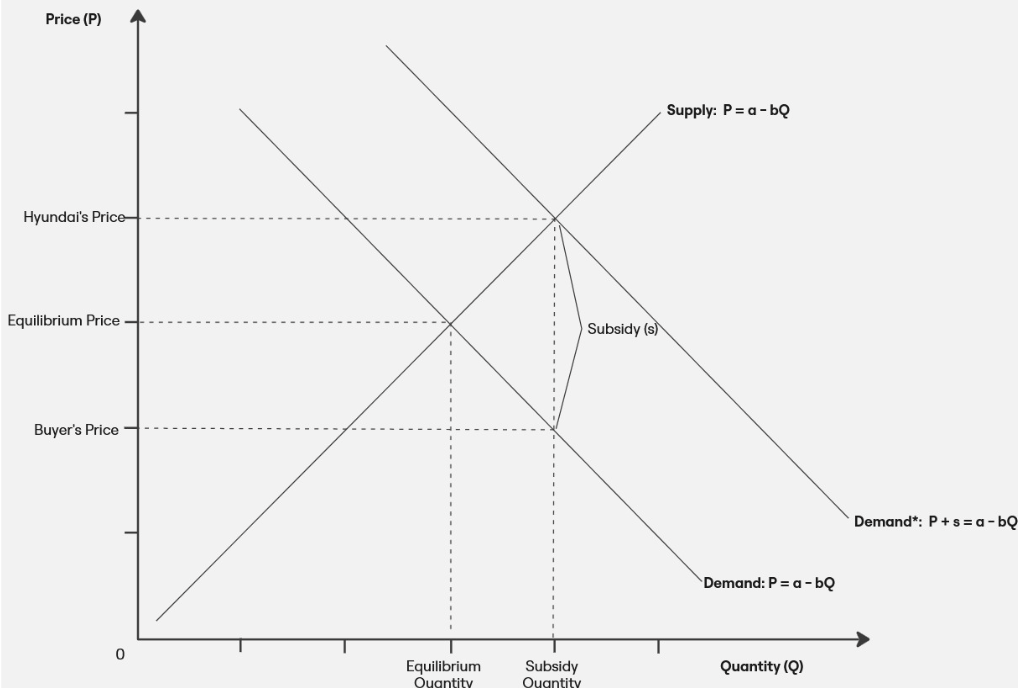

Demand-Side Effects

A tax credit functions as a demand-side subsidy: it reduces the effective price paid by consumers, shifting demand outward. The economic effect is shared between buyers (who pay less) and producers (who can sell more, and at higher quantities). When the subsidy is removed, demand contracts, prices to consumers rise, and quantity supplied falls. Buyers priced out either substitute toward subsidized EVs or toward non-EV alternatives.

What's interesting in the Ioniq 5's case is that the simple model didn't fully play out. EV sales grew 35% from 2022 to 2023 industry-wide. Ioniq 5 sales — without the credit at the time — grew 47.6%. The Model Y, which qualified, grew 70.9%.

| Make & Model | 2022 Units | 2023 Units | YoY Growth | Industry Avg |

|---|---|---|---|---|

| Hyundai Ioniq 5 | 22,982 | 33,918 | 47.6% | 35% |

| Tesla Model Y | 225,799 | 385,897 | 70.9% | 35% |

The Model Y's outsized growth is consistent with subsidy eligibility being a major contributor — but the Ioniq 5 still beat industry average without it, suggesting Hyundai's brand, dealer incentives, and lease structures absorbed some of the disadvantage. Hyundai's reliance on lease incentives and dealer discounts during this period exemplifies a reactive strategy in a high-elasticity market.

Why Elasticity Matters Here

EV demand is relatively elastic (>1) because EVs remain a discretionary purchase for many buyers and substitutes — gas-powered cars, hybrids, other EVs — are readily available. In an elastic market, subsidies are a powerful lever: they materially compress the effective price gap between EVs and traditional vehicles, stimulating demand. Conversely, withdrawing the subsidy can severely hurt demand. The more expensive the EV, the greater the impact, because the absolute dollar gap (relative to substitutes) widens. The Ioniq 5 was actually well-positioned to weather subsidy loss compared to higher-priced EVs.

Supply-Side Effects

The IRA is usually framed as a demand-side policy, but its design also forces a supply-side response. By tying eligibility to North American final assembly, the policy effectively requires automakers serving the U.S. EV market to relocate or build production capacity domestically — or accept a structural pricing disadvantage.

Production Relocation as a Long-Run Supply Shift

Hyundai's $7.6B investment in HMGMA in Bryan County, Georgia, is a textbook example of a firm strategically altering its long-run production function in response to policy incentives. The facility is expected to produce ~300,000 EVs annually initially, scaling to a potential 500,000.

Economically, relocating production from international locations to the U.S. reduces long-run average costs through shorter supply chains, lower tariffs, and reduced geopolitical risk. The supply curve shifts outward in the long run, enabling higher production volumes at lower marginal costs. The Ioniq 5 had previously operated at a higher marginal cost structure due to import taxes, shipping costs, and ineligibility for consumer credits. Localization moves Hyundai closer to its optimal MR=MC equilibrium.

Battery Supply Chain Realignment

Hyundai also restructured its battery supply chain through a partnership with SK On, investing in domestic battery plants and localizing critical components. Battery components represent 30–40% of EV production costs, so this shift materially affects marginal and average cost structures. Vertical integration through the SK On partnership reflects classic cost-minimization in supply-chain management — and ensures consistent compliance with IRA critical-mineral and battery-component sourcing rules.

Short-Run vs. Long-Run Elasticity

In the short run, Hyundai's supply curve is relatively inelastic. Production lead times, fixed capital requirements, and limited domestic input availability prevent quick output adjustment in response to demand shifts. Once HMGMA reaches scale, long-run elasticity improves significantly: Hyundai can respond more rapidly to price and market shifts, represented by a flatter, outward-shifting long-run supply curve. The structural improvement in long-run elasticity is the deeper economic rationale behind the upfront capital commitment.

Competitive Dynamics

Restored Price Parity

Once the Ioniq 5 regained eligibility through HMGMA assembly, its effective price dropped to roughly $35,100 — below the Model Y's $37,490 post-credit effective price. Hyundai didn't just close the gap; it inverted it. For the price-sensitive buyer comparing the two SUVs head-to-head, the Ioniq 5 became the cheaper option for the first time.

Cross-Price Elasticity

The restoration of the credit also intensified cross-price elasticity — the tendency of consumers to switch between similar EVs based on price. Industry data showed Ioniq 5 sales surging in 2024 as eligibility approached. Buyers who might otherwise have selected a Model Y became more likely to consider the Ioniq 5 as the effective price gap narrowed and then reversed. BloombergNEF noted that "alternatives [are] becoming more prominent, especially as EV makers target more price-sensitive and larger portions of the car market."

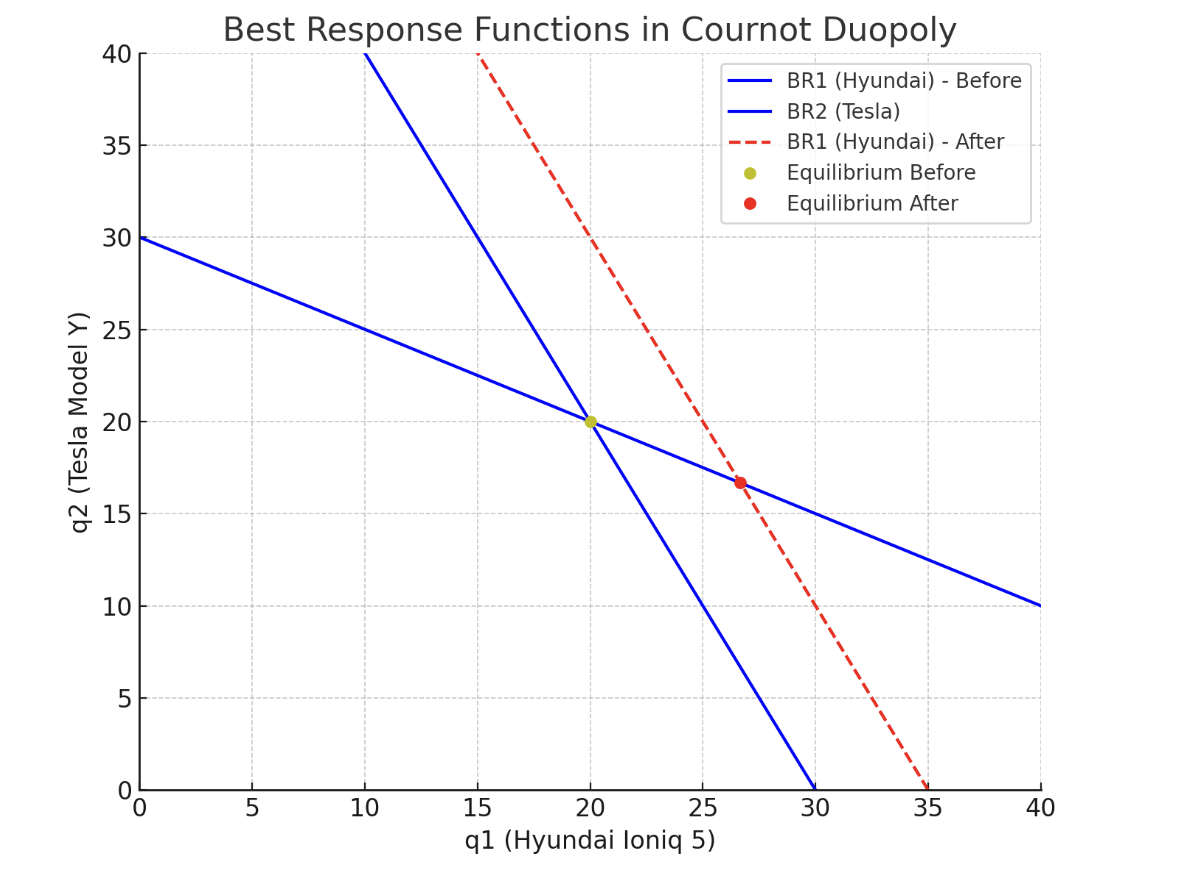

Game-Theoretic Framing

Hyundai's investment in U.S. production can be read through a Cournot lens. In Cournot competition, each firm chooses output in response to anticipated rivals' production decisions. Hyundai's decision to ramp domestic capacity and secure tax-credit eligibility is a best response to Tesla's incumbent advantage of qualified domestic production. The result is a market equilibrium where each automaker's investment and output decisions are mutually responsive — and no firm can unilaterally improve its outcome without inducing competitive response.

This reframes the HMGMA investment from "compliance with IRA" to "structural repositioning within an evolving competitive equilibrium." It also makes the strategy more sensitive to policy stability: the equilibrium that justifies the investment depends on the credit continuing to exist.

Broader Policy Implications

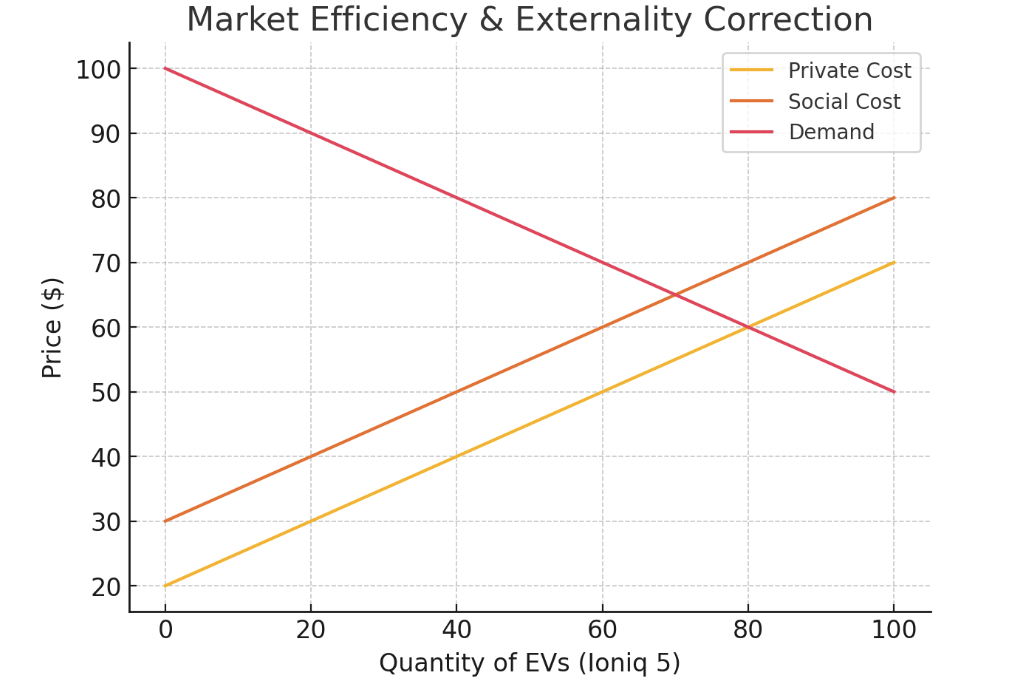

Externality Correction

The credit addresses a well-known externality: GHG emissions from internal combustion vehicles. By lowering the effective price of EVs, the policy increases the share of cleaner vehicles in the U.S. fleet, supporting climate goals. The economic rationale is standard externality correction — internalizing costs that the market would otherwise leave unpriced.

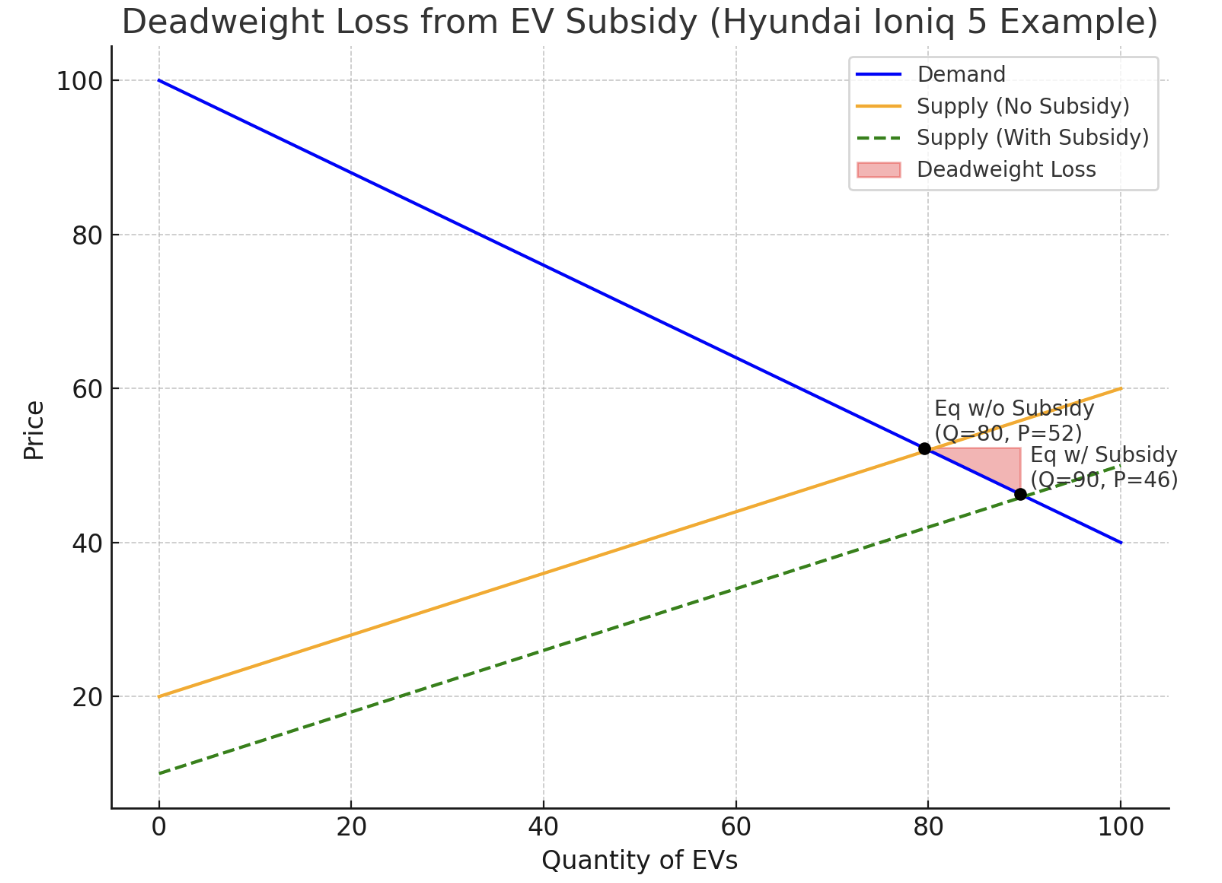

Deadweight Loss

Subsidies are not free of distortion. Recent analyses suggest only 23–33% of EV purchases incentivized by the subsidies are genuinely incremental — the rest would have happened anyway. The remaining share represents deadweight loss: subsidy dollars that displaced market-driven purchases without changing aggregate behavior. Subsidies can also delay price-based competition and slow innovation by reducing the pressure on automakers to bring costs down.

Policy Uncertainty and Stranded Investment Risk

The most pressing risk, post-2024, is policy uncertainty. Proposed legislation — the so-called "One Big Beautiful Bill" — would eliminate the EV tax credit entirely. If enacted, the policy lever that justifies HMGMA's economics partially disappears. Hyundai's $7.6B investment doesn't become worthless (the plant still produces vehicles), but the strategic premium it was designed to capture — credit eligibility and restored price parity — would evaporate. This is the canonical "stranded investment" risk in policy-driven capital allocation.

Strategic Implications for Hyundai

Translating the analysis into actionable implications for Hyundai's strategy team:

Hedge against subsidy repeal explicitly. HMGMA's economics depend on more than one revenue stream. Even without the credit, the plant should remain economically viable through (a) supply-chain cost savings versus imported assembly, (b) reduced exposure to tariffs and geopolitical risk, and (c) shorter logistics timelines. The strategic narrative around HMGMA should emphasize these structural advantages, not just credit eligibility, so that the investment story holds under both policy scenarios.

Lean on the lease loophole as bridge pricing. Even when the credit was unavailable for direct retail purchase, leasing arrangements continued to qualify because the credit could be claimed at the corporate level and passed through to lessees. Hyundai used this aggressively during the eligibility gap. If the credit is repealed for retail buyers but commercial-lease provisions remain, the lease channel becomes the primary pricing lever and should be operationalized accordingly.

Communicate the price-parity advantage now. With the post-credit Ioniq 5 priced below the post-credit Model Y, Hyundai has a window where it is the cheapest premium electric SUV in the U.S. market. Marketing should be aggressive about this comparative pricing — particularly to first-time EV buyers who anchor on Tesla pricing as the reference point. The window may close if the credit is repealed.

Use Metaplant flexibility as optionality. The 300K-to-500K annual capacity at HMGMA gives Hyundai meaningful production flexibility. Under continued credit availability, ramp aggressively to capture share. Under credit repeal, throttle production to maintain margins and avoid demand-driven price compression. The plant's modularity is itself a strategic asset under policy uncertainty.

Treat policy advocacy as a competitive lever. Because the IRA structurally favors domestic assemblers (which Hyundai now is), Hyundai's interests now align with continued credit availability — the same way Tesla's, GM's, and Ford's do. Joining industry coalitions to advocate for IRA continuity is a low-cost, high-value lever once the domestic plant is operational.

Strategic Takeaways

A few takeaways extend beyond Hyundai specifically:

Policy-driven subsidies trigger structural — not just behavioral — responses in elastic markets. The Ioniq 5 case demonstrates that automakers don't just adjust prices in response to subsidy availability; they relocate production, restructure supply chains, and lock in long-run cost positions. The supply-side response is often larger and more durable than the demand-side response the policy was designed to produce.

Eligibility cliffs create concentrated investment behavior. When a policy creates a binary eligibility line (in this case, "final assembly in North America"), firms cluster capital expenditure on the domestic side of that line. The result is a wave of domestic capacity build-out — beneficial for industrial policy goals, but also a vector for stranded-investment risk if the underlying policy changes.

Competitive equilibria built on policy assumptions are fragile. The Cournot-style equilibrium between Hyundai and Tesla post-HMGMA depends on the EV tax credit continuing to exist. When core inputs to a competitive equilibrium are politically determined, the equilibrium itself becomes a policy variable rather than a stable strategic anchor.

Elasticity intuition matters more than absolute price levels. Whether a subsidy meaningfully changes consumer behavior depends on the elasticity of the demand it's aimed at. EVs are highly elastic; subsidies move the needle. For demand that's already inelastic, subsidies primarily transfer wealth without changing behavior — which is where deadweight loss is largest and political backlash is most likely.

Hyundai's experience is, in this sense, not just an EV story. It's a clean illustration of how policy, supply structure, and competitive strategy interact in markets where the rules of the game are themselves in flux.